3 vital ways stagflation could affect your wealth in 2023 and beyond

14 March 2023

As you may already know, UK inflation has reached a 40-year high in the past 12 months. In its most recent report, the Office for National Statistics (ONS) says inflation reached 10.4% in the year to February 2023.

Indeed, there is no doubt that your spending power has been affected by the increasing rate of inflation, which signifies rises in the cost of everyday goods and services across many industries.

One major contributing factor to today’s high inflation rate is supply chain issues. These have been largely caused by:

- Russia’s invasion of Ukraine. With energy and other supplies cut off from key exports as a result of the war, prices saw a dramatic increase in 2022 – some of which have remained high at the start of 2023.

- The Covid-19 pandemic. During the height of the pandemic, global exports and imports slowed down. What’s more, the UK and US governments printed money to inflate the economy – also known as “quantitative easing” – which has also contributed the inflationary conditions we are experiencing.

One word you may have seen in the news recently is “stagflation” – and you could be wondering what it means, and how it differs from inflation.

Stagflation describes a combination of high inflation and a slowing, stagnating, or declining economy. It could be said that this is the “perfect storm” for economic hardship, as prices are continuously rising while jobs and business performance are in poor stead.

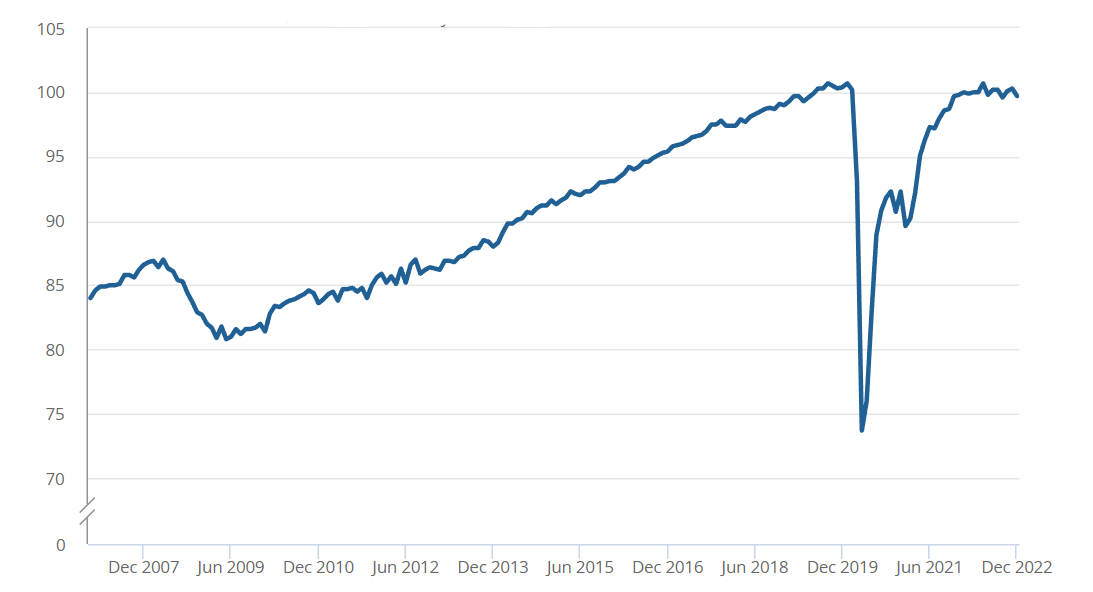

According to the ONS, UK Gross Domestic Product (GDP), meaning the measure of the country’s economic health, declined by 0.5% in December 2022, after being “flat” for the three months prior. Overall, GDP grew by just 4.1% in 2022, down from 7.4% growth in 2021.

The below graph shows how UK GDP experienced a significant dip during the pandemic – and while it rebounded quickly, it has stagnated over the last year.

Source: ONS

So, combining a crawling economy with high inflation, stagflation could have an impact on your wealth this year. Here are three vital things you should know about how stagflation might affect you.

1. You may find it harder to cover costs

When inflation rises, the truth of the matter is: you may need more money to achieve the same lifestyle you had before.

Indeed, you may already have noticed your regular expenditure falling short of what’s needed in the past year, as the UK’s cost of living crisis has put pressure on household spending.

When combined with a stagnating economy, your slowed spending power could be felt even more sharply. If you run a business, are in search of new employment, or are looking for a pay increase in your current role, all of these endeavours could be made more difficult by slow GDP growth.

So, while usually individuals might ask for a pay rise or raise business prices to match rising inflation, if these avenues are more difficult to pursue you could find yourself needing to cut back on spending altogether.

2. Stagflation could dampen your saving power

In a similar vein to the above point, stagflation can not only have an effect on your spending, but on your saving too.

If you need more cash to cover the same costs due to inflation reaching double figures, this may leave less for you to save each month.

Indeed, a slowing economy and soaring inflation could weaken your ability to:

- Keep up your pension contributions

- Build a nest egg for the next generation

- Make further investments to grow and diversify your portfolio

- Expand your property portfolio

- Maintain an emergency cash fund.

So, in this period of stagflation, it could be hugely beneficial to check in with your financial planner. We can help you prioritise the financial factors that mean the most to you, and make a plan to protect your wealth through the potentially challenging year ahead.

Please note, investments carry risks. The value of your investment (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

3. You could take on more debt to keep your wealth afloat

Finally, during a period of stagflation, it could be very tempting to take on more debt – be it a more expensive mortgage, additional credit card loans, or corporate debt if you are a business owner.

While there is nothing wrong with keeping your finances buoyant through what should be a temporary phase for the UK economy, it is crucial to understand the risks of taking on higher debt in a time of stagflation.

In times of economic difficulty, household debt typically rises. For instance, after the 2008 financial crash, the House of Commons Library reports household debt peaked at 155.6% of disposable income. In Q3 2022, household debt stood at 133.8% of disposable income.

Now, with the base rate standing at 4.25%, and Moneyfacts reporting the average two-year fixed mortgage rate is 4.64% as of 16 March 2023, the bottom line is: borrowing more might be an expensive move at the moment.

Please note, your home maybe repossessed if you do not keep up repayments on your mortgage or other loans secured on it.

Fortunately, working with your financial planner to plan for the coming months and years can alleviate your worries.

Sometimes, taking on more debt is inevitable – but with the right guidance, you could find it entirely manageable. Or, with the help of a professional, you might find that there are ways to continue covering costs and saving for the future without taking out another loan.

Ultimately, it is important to remember that this period of stagflation is not permanent. If you find yourself worrying about how it will affect your finances, speaking with a financial planner could bring you invaluable peace of mind.

Get in touch

To discuss the effects of stagflation on your income, savings, investments, and overall financial plan, get in touch today. Email info@depledgeswm.com or call 0161 8080200.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.