Your Q2 2026 global market update

10 July 2026

Each quarter, we share a global market update, summarising significant events across major stock market indices.

Compared to the first quarter of the year, when investors saw plenty of volatility, Q2 2026 proved positive for global markets – despite ongoing geopolitical uncertainty.

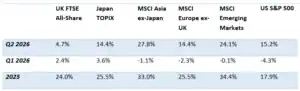

Below is a table showing the performance of six key world indices in Q2 2026 and in the previous year.

Source: JP Morgan

Keep reading for further insight into some of the main events influencing these results.

The second quarter of 2026 may be one of the strongest periods for US equities in recent memory

Although inflation, interest rates, and geopolitical uncertainty continued to cause some concern, investors were not deterred.

As a fragile peace agreement has helped calm the situation in the Middle East, markets have also benefited from positive returns from AI-related stocks.

As a result, following disappointing results in the first quarter of 2026, many of the major markets ended the quarter on record highs.

The MSCI All World rose 14% for the quarter, marking the best second-quarter performance in six years. Meanwhile, the S&P 500 ended the quarter 15.2% higher, despite a rough start to June.

Indeed, reports suggest that Q2 2026 may be remembered “as one of the strongest periods for US equities in recent memory”.

UK

Following a sharp dip in late March, caused by escalating events in the Middle East, UK stock markets showed relatively stable growth throughout the second quarter of 2026.

When Prime Minister Keir Starmer announced his resignation on June 22, markets reacted to the news relatively calmly – mainly because the news had been trailed for several weeks and so came as no surprise.

With Andy Burnham widely expected to step up as leader of the Labour Party and become the next prime minister, changing economic policies could lead to some volatility in the coming weeks.

Although economists had predicted a rise in inflation, according to the Office for National Statistics, inflation remained static at 2.8% in the 12 months to May 2026.

Following this news, the Bank of England held interest rates at 3.75%, citing ongoing disruption to energy supply caused by the war in the Middle East, which has led to rising prices and higher household bills.

Meanwhile, UK house prices have stalled, with agents warning there may be a summer slump. According to the Guardian, the average price of a typical UK home edged down to £277,484 in June from £278,024 in May.

US

For US stock markets, geopolitics and technology continued to be the biggest factors affecting performance.

As the war in the Middle East began to de-escalate, with the US and Iran signing an interim peace agreement, Brent crude prices started to fall after peaking at USD 120 per barrel in April. In the immediate aftermath, Brent crude dropped more than 5% to $82.84 (£61.70) a barrel.

For the S&P 500, the first quarter of 2026 benefited from one of the strongest earnings seasons in recent years. According to JP Morgan, “85% of companies beat consensus expectations, the most since 2021 and well above the long-term average of 73%”.

AI is also still helping to elevate technology stocks, supporting earnings growth across multiple sectors – with banks benefiting from AI-driven activity and demand for electrical equipment boosting industrials.

Overall, US equities gained 15% during the second quarter of the year.

In the wider economy, US consumer prices rose by 0.5% in May – a year-on-year increase of 4.2% – primarily driven by a 7.0% increase in petrol prices.

However, as vessels have started moving through the Strait of Hormuz, oil prices should start to fall in the coming months.

Unemployment is at 4.3%, and there’s been a healthy growth in private payrolls, and yet average hourly earnings for all workers rose just 3.5% in May – the second-smallest gain in five years.

In light of all of this, the Fed kept interest rates at 3.50%–3.75%, although the statement was dramatically shorter with a noticeable absence of any bias towards future cuts.

Eurozone

Once again, the improving situation in the Middle East and strong economic sentiment helped European markets rally.

In the second quarter of 2026, the MSCI Europe ex-UK returned 14%.

In other news, the European Central Bank (ECB) announced the first rate change in 11 months – increasing the key interest rate to 2.25%.

Because the move had been widely anticipated, European bond markets responded well – outperforming the global bond index.

Meanwhile, inflationary pressures in the region remain moderate: headline CPI increased to 3.2% in May while core CPI increased only marginally to 2.5%.

Asia

As shown in the table above, MSCI Asia ex-Japan delivered the strongest performance during the second quarter of the year, returning almost 28%.

This was primarily supported by Korea (+88%) and Taiwan (+49%), thanks to investor demand for electrical equipment companies and semiconductors.

Indeed, JP Morgan reports that SK Hynix tripled in value while Samsung Electronics doubled, helping to deliver the best quarterly performance for Korean equities since 1998.

In Q2 2026, both companies now enjoy a market cap of more than US$1 trillion.

Meanwhile, Chinese exports jumped 19.4% year-on-year in May, with chip exports more than doubling.

In economic news, inflation pressure led to Japan’s central bank hiking interest rates from 0.75% to 1%. Though the increase is small, it’s the highest rate in Japan since 1995.

Speak to us about carefully managing your investments

The second quarter of 2026 has been overwhelmingly positive for investors.

As events continue to unfold and influence markets in the coming weeks or months – particularly in the UK with a change in leadership – we are here to guide you through periods of uncertainty and ensure you remain informed.

No matter where you are on your investment journey, our team can help you build and manage a diversified portfolio designed to weather market volatility while allowing you to achieve your long-term goals.

Email [email protected] or call 0161 8080200.

Please note

This article is for general information only and does not constitute advice. The information is aimed at retail clients only.

All information is correct at the time of writing and is subject to change in the future.

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

Investments should be considered over the longer term and should fit in with your overall attitude to risk and financial circumstances.