How proposed Inheritance Tax rule changes on pension wealth could affect your estate plan

5 February 2026

Pensions have traditionally fallen outside your estate. If you passed away today, your pension would not form part of your estate for Inheritance Tax (IHT) purposes.

However, from 6 April 2027, that will no longer be the case, as unused pensions and death benefits will be included within the IHT net.

Here’s what’s happening and how it may affect your estate plan.

Inheritance Tax changes on unused pensions could lead to effective tax rates of up to 67%

From 6 April 2027, in a move designed to deliver a fairer and less economically distortive tax treatment of inherited wealth and assets, unused pension funds and death benefits will be included in an individual’s estate upon death.

As such, pension savings will become subject to IHT at a rate of 40% on amounts exceeding the nil-rate band – £325,000 in the 2025/26 and 2026/27 tax years.

In some cases, beneficiaries receiving pension savings may also be liable to Income Tax.

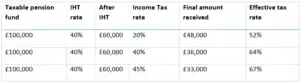

For example, a taxable pension fund of £100,000 could incur an effective tax rate ranging from 52% to 67%, depending on the Income Tax bracket of the beneficiary, on death after age 75.

The table below shows how IHT and Income Tax could combine to significantly increase the effective tax rate on inherited assets – particularly where income is taxed at higher or additional rates.

Your estate plan may have been devised around the belief that your pension would be a helpful, tax-efficient way to transfer your wealth. If so, the current proposals may require you to rethink your strategy and could lead you to adjust how you use your pension savings.

Bear in mind that tax treatment will depend on individual circumstances and may change in the future. Plus, as a long-term investment, pension savings may fluctuate and can go down. This may affect the level of pension benefits available, and past performance isn’t a reliable indicator of future performance.

Baroness Altmann is taking a stand, asking the government to “rethink their plans”

House of Lords member Baroness Ros Altmann has been vocal about her concerns surrounding the planned changes, saying they “could kill off modern pensions”.

An FTAdviser report highlighted the possibility that imposing IHT on pensions could put people off saving for their long-term futures, with Altmann warning that the policy could “damage the future of pensions in this country”.

She’s also shared concerns that instead of closing a loophole used by wealthy families, the proposed changes could harm ordinary families.

While actively lobbying the government to roll back this decision, she does present an alternative option, arguing that a flat-rate levy on unused pensions would be a simpler way to reform the system.

To this end, Altmann is campaigning for a 15% flat-rate charge that would apply to all pensions, payable on death regardless of an estate’s IHT position. To simplify administration, she recommends that the fee be paid from the pension fund at source by the provider.

If you agree with the principle, we’d encourage you to support Baroness Altmann’s proposition and write to your MP.

We recently attended an event where Altmann shared her thinking, and would be more than happy to explain her alternative proposition and why we support her views on IHT and the future of pensions. If you wish to discuss this in more detail, please don’t hesitate to get in touch.

The £2.5 million cap on Business Relief and Agricultural Relief will also reduce tax efficiency

Another area of change you may need to consider is the new cap on 100% relief for Business Relief (BR) and Agricultural Relief (AR).

From April 2026, 100% relief will be limited to the first £2.5 million of qualifying assets – up to £5 million if you’re planning as a couple.

Amounts above this threshold will be eligible for relief at 50%. In other words, IHT would be charged at 20% instead of the full 40%.

As Baroness Altmann warns, these changes could affect tax-advantaged schemes such as Venture Capital Trusts (VCTs) and the Enterprise Investment Scheme (EIS).

If you invest either one of these vehicles, are a business owner, or use complex trusts to mitigate exposure to IHT on your estate, you may need to review your existing plans before the new tax year starts on 6 April 2026.

Please remember that both the EIS and VCTs are higher-risk investments, and typically only suitable for UK-resident taxpayers who are able to tolerate increased levels of risk and are looking to invest for five years or more. Furthermore, historical or current yields should not be considered a reliable indicator of future returns, as they cannot be guaranteed.

Share values and income generated by these high-risk investments can go down as well as up, meaning you may get back less than you originally invested. These investments are also highly illiquid, which could make it difficult for you to realise your shares at a value close to the value of the underlying assets.

While both investment vehicles offer tax incentives, tax levels and reliefs could change, and the availability of tax reliefs will depend on individual circumstances.

Bespoke financial planning can help you transfer your wealth tax-efficiently

While the IHT rule changes may affect your family, we’re here to help you focus on your personal long-term goals and adapt your financial plan.

Last September, we published an article about gifting surplus income, which allows you to make unlimited IHT-free gifts to your beneficiaries.

This is just one strategy that may help you to mitigate the eroding effects of IHT on your estate.

If you’re concerned about how the upcoming changes discussed here may affect you and your family, we can help you:

- Review your estate plan in light of the proposed IHT changes

- Consider strategies that could help to reduce the value of your estate before your death

- Create a bespoke plan that takes all the upcoming Budget changes into consideration.

From utilising gift allowances to setting up trusts and more, we’ll ensure more of your hard-earned wealth passes to the people you care about.

Get in touch

To speak to an independent financial planner about IHT, or any other financial matter, email [email protected] or call 0161 8080200.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate estate planning.