Could you be one of thousands paying too much tax on your pension?

10 March 2026

Since 2015 when the government introduced Pension Freedoms, you’ve had more flexibility in how you can access your pension. This means that buying an annuity isn’t the only option – you can also use flexi-access drawdown to withdraw lump sums as and when you feel they’re needed.

This is good news because many retirees now enjoy more control over their retirement income.

It’s another story when it comes to tax, however, as the change has created some problems.

Indeed, consumer magazine Which? reports that people have reclaimed more than £1.5 billion since the introduction of Pension Freedoms.

In the final quarter of 2025 alone, HMRC refunded £46.2 million to pension savers who had been overtaxed on their pension withdrawals. 13,600 reclaim forms were filed and the average refund per claim was £3,300.

With such significant sums involved, read on to learn more about how overtaxation can occur and what to do if you think you might be owed a refund.

The way HMRC measures your income and assigns your tax code has been slow to catch up

If you’ve just started receiving your private pension, HMRC will now automatically update your tax code. If your tax code is changed, HMRC should notify you – by letter or digitally.

However, problems remain for those making one-off ad-hoc withdrawals, as payments can still be taxed using emergency codes.

In some cases, you may end up paying more tax than necessary.

While taking a small “notional” withdrawal first may help HMRC apply the correct code to a larger second payment, it may not suit your goal.

Remember, a pension is a long-term investment; you can’t normally access your savings until 55 (57 from April 2028). The money in your pension is invested, so the value may fluctuate and can go down. This may affect the level of pension benefits available.

Why you may be charged too much tax if you withdraw a large lump sum from your pension

One of the benefits that drawdown typically offers is the option to take a tax-free lump sum from your pension fund when you reach retirement, with the remainder charged as income at your marginal rate.

If you’ve recently retired and don’t yet have a tax code, HMRC may assign you an emergency tax code and assume you’ll make the same withdrawal every month.

However, if you’ve taken out a lump sum for a one-off purchase, or to provide income that’s intended to last for some time, you’re unlikely to make the same level of withdrawals every month.

This is why so many retirees end up overpaying tax, particularly when they first start to access their pension.

Bear in mind that the tax implications of pension withdrawals will be based on your individual circumstances. Thresholds, percentage rates, and tax legislation may change in subsequent Finance Acts.

Keep track of your retirement income and taxes to check if you have overpaid

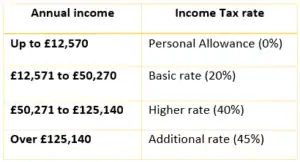

After you have taken the full tax-free lump sum available, the same rates of Income Tax apply as they do to employed income.

In 2025/26 and 2026/27, these are:

Keeping track of the income you’ve taken in retirement and the amount of Income Tax you’ve paid will make it easier to spot if you have overpaid tax in a given year.

Remember to include all types of income in your calculations, including:

- State Pension

- Rental income

- Pension withdrawals

- Employment earnings

- Dividends that exceed the Dividend Allowance.

If you have multiple income streams in retirement, it can be more challenging to keep track of how much tax you need to pay. Keeping clear records and checking your finances on a regular basis can be a big help.

If in doubt, please get in touch. We’ll help you understand what tax you may owe and point out areas where there may be potential to make your finances more tax-efficient.

Remember to reclaim any overpaid tax you are owed

If you notice that you have overpaid tax, you can reclaim the excess from HMRC. The correct form will depend on your circumstances.

- Use form P55 if you’ve flexibly accessed part of your pension and aren’t withdrawing regular payments.

- Use form P50Z if you’ve stopped working and have accessed all of your pension.

- Use form P53 if you’ve taken a small lump sum from your pension.

In all cases, you can either complete the form online or print and return a hard copy to HMRC.

Get in touch

Getting money out of your pensions and investments in retirement can be a minefield.

We’re here to help you create a personalised withdrawal strategy that minimises your tax liability while providing the cashflow you need.

To find out more about how we could help you, please email [email protected] or call 0161 8080200.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.

The Financial Conduct Authority does not regulate tax planning.