Business owner? Tax changes may mean it’s time to rethink how you pay yourself

11 June 2026

A combination of increasing tax rates, frozen thresholds, and changes to National Insurance have all conspired to make it more costly for small business owners to pay themselves.

Keep reading to understand the detail and how we can help you ensure you’re making the most of various tax-efficient opportunities.

3 taxes and costs that may influence how you pay yourself in 2026/27

As you read, please bear in mind that levels, bases of, and reliefs from taxation may be subject to change and their value will depend on your individual circumstances.

1. Static Income Tax rates

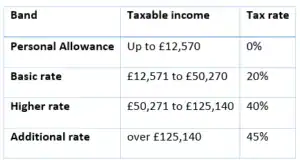

Income Tax brackets have remained stable, and the tax-free Personal Allowance (currently frozen until 2031) is £12,570.

While there’s been no direct rise in Income Tax, frozen thresholds do raise concerns about fiscal drag. As inflation and higher costs of living mean you’ll likely need to pay yourself more, tax freezes could drag you into a higher tax bracket.

2. Although the Dividend Tax Allowance has dropped in recent years, dividends still beat income

While the Dividend Allowance has reduced in recent years, you can still take up to £500 tax-free in 2026/27.

Beyond the £500 allowance, you must pay tax on any dividends you receive from your limited company.

The rate you pay will depend on your Income Tax band:

- Up to £50,270 (basic rate) – 10.75%

- £50,271 – £125,140 (higher rate) – 35.75%

- £125,140 and above (additional rate) – 39.35%

As the Dividend Tax rates are lower than the Income Tax rates, paying yourself through dividends instead of salary could prove more tax-efficient.

Another bonus is that you won’t pay National Insurance on dividends from your business, leading nicely onto how National Insurance plays into the calculations…

3. National Insurance contributions can add up

In addition to Income Tax, employees (including directors) and their employers must make Class 1 National Insurance contributions (NICs) on earnings above certain thresholds.

When paying yourself a director’s salary, you’ll pay 8% employee NICs on earnings above £12,570 each year (NIC primary threshold) up to £50,270 per year (NIC upper earnings limit).

On any portion of income that’s above the upper earnings limit (£50,270), you’ll pay a reduced rate of 2%.

Your company will also be liable to pay 15% employer (secondary) National Insurance contributions on your salary income above £5,000 per year (NIC secondary threshold).

Although HMRC lists current and previous NIC rates and thresholds online, it can be a lot to figure out when you’re busy running a business. We’re here to help you navigate this and other tax complexities – to find out more, please get in touch.

Get in touch

If you’d like help reviewing all available options to ensure you’re drawing a tax-efficient income from your business, please email [email protected] or call 0161 8080200.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

The Financial Conduct Authority does not regulate tax advice.