Revealed: How the finer details of Inheritance Tax on pensions could affect you

11 June 2026

Less than a year from now, unused UK pension savings will be subject to Inheritance Tax (IHT).

From April 2027, should your total assets, including your pension savings, breach the IHT nil-rate band, your estate could be liable to pay IHT.

Thresholds, rates, and exemptions – a quick Inheritance Tax recap

In the current 2026/27 tax year:

- Your estate will typically only be subject to IHT if it exceeds the nil-rate band of £325,000.

- Leaving your home to your children or grandchildren and using the residence nil-rate band of £175,000 could take your total IHT-free threshold to £500,000.

- Any wealth that exceeds these two nil-rate bands is usually taxed at 40%, but if you leave 10% or more of your estate’s value to charity, this rate may be reduced to 36%.

- Your estate won’t usually be subject to any IHT if you leave all your assets to your spouse, civil partner, or charity organisations.

- Any unused nil-rate bands can be added to your spouse or civil partner’s threshold when you die.

- Both the nil-rate band and residence nil-rate band thresholds are currently frozen until April 2031.

While levels, bases of, and reliefs from taxation may be subject to change and their value depends on your individual circumstances, once pensions come into scope, your estate may become more likely to be liable to IHT.

Indeed, when the new rules come into force, the government expects:

- 10,500 estates will have an IHT liability where they previously would not

- 38,500 estates will pay more IHT than previously

- The average IHT liability will increase by roughly £34,000.

If your pension savings will expose your loved ones to a potential IHT charge, you may wish to revisit your estate plan.

It might also be useful to understand how HMRC will implement the new rules and how they may affect your family and estate executors, so here are four key questions answered.

4 key questions about how the new rules may affect your estate, executors, and family

1. When will the new rules come into effect

UK pension savings could become liable to IHT from 6 April 2027. In the event that a pension scheme member dies before 6 April 2027, pension savings won’t be liable to IHT – even if pension benefits are paid to beneficiaries after this date.

2. Who will be responsible for calculating pension savings and Inheritance Tax owed?

HMRC states that “personal representatives will be responsible for reporting and liable for paying any Inheritance Tax due on notional pension property.”

This means that executors and administrators will need to work closely with pension providers to identify and obtain valuations for all private pension arrangements.

Your executors must then report findings to HMRC.

3. How and when will Inheritance Tax be collected?

As with the existing process, any IHT owed on pensions will be due six months after the date of the death.

While you have until the end of the sixth month to pay, if you’re late paying, late payment interest will be added to the outstanding amount owed.

Personal representatives will be responsible for paying IHT.

However, in some circumstances – for example, where pension property is vested in a beneficiary – the pension scheme provider may become jointly and severally liable if they fail to action a valid withholding notice or payment notice.

As pension funds are often only released after probate and IHT is usually required to be paid before probate is settled, this could create a liquidity issue. In these cases, executors will have the authority to request that pension fund administrators pay IHT before releasing the remaining funds.

4. What could I do to make life easier for my executors?

As is so often the case, preparation is key. When it comes to your estate plan, keeping clear and accurate records could make all the difference to your executors and family after you’re gone.

One of the best ways to help ensure your family have what they need to sort out your estate and minimise stress and delay is to create a comprehensive emergency file.

Along with contact information for your solicitor, financial planner, and accountant, this should also include your legal documents, financial information, and insurance details.

Including details of all your pension savings could save your family a lot of time – especially if you’ve accrued several different pension pots during your lifetime. Make a note of the provider, and add each annual statement to the folder as and when you receive it.

Having immediate access to the most recent annual statement will quickly tell your family the value of your pension, while giving them precise information about the pension provider, along with up-to-date contact details.

Inheritance Tax may create a double taxation issue for some beneficiaries

Now you understand how inherited pension savings may be subject to IHT at 40%, there’s another taxing issue to consider, as some beneficiaries may also be liable for Income Tax.

This double taxation could mean your loved ones end up paying an effective tax rate of 67% on inherited pension wealth.

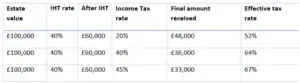

For example, a taxable pension fund of £100,000 on death after age 75 could incur an effective tax rate of:

- 52% for basic-rate taxpayers

- 64% for higher-rate taxpayers

- 67% for additional-rate taxpayers.

The table below shows how IHT and Income Tax could combine to significantly increase the effective tax rate on inherited assets – particularly where income is taxed at higher or additional rates.

Bear in mind that levels, bases of, and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor. Plus, as a long-term investment, pension savings may fluctuate and can go down. This may affect the level of pension benefits available, and past performance isn’t a reliable indicator of future performance.

We’re here to help you and your family navigate the incoming changes

If you’ve been viewing your pension as a useful way to transfer wealth tax-efficiently to your beneficiaries, now is a good time to review your plan.

From using all your gifting allowances to drawing additional income to support your loved ones, we can advise you on potential strategies to ensure more of your hard-earned wealth passes to the people you care about.

If you’d like to discuss what methods might be appropriate for you and your family, please get in touch.

Email [email protected] or call 0161 8080200.

Please note

This article is for general information only and does not constitute advice. The information is aimed at individuals only.

All information is correct at the time of writing and is subject to change in the future.

The Financial Conduct Authority does not regulate tax advice or estate planning.